4 Methodology

Our methodology is based on individual level surveying based on a US-EU harmonized model of the music industry. Our survey is unique in many ways, and whenever it overlaps with IFPI’s, CISAC’s and Live DMA’s data collection, it is complementing them, and adds further value to these organizations members, too. It also combines very well with audience surveys.

We are asking music professionals, mainly working in microenterprises, about their market knowledge. The term music professional refers to that fact that professional musicians often perform educational, managerial, engineering or other duties besides their artistic expression. Since most music professional work in microenterprises, or as freelancers, they usually do not participate in economic statistical surveys, and their problems remain hidden from government officials and the general public. This is why we designed a complicated, boring, but necessary individual-level survey. We want to show the economic and social conditions of music professionals. Our methodology follows US standards, first adopted by the EU for Europe, and then further adopted by CEEMID for less developed markets.

4.1 What Is A Music Professional?

Given that the average size of creative enterprises in Europe is less than two people, musicians are forced to do several very different things. In the 20th century, larger companies, especially record labels had the necessary marketing, management, and engineering resources. In the 21st century many musicians need to master all of these skills to a certain extent – at least to the extent that they can hire others, mainly freelance music professionals to help them out.

Official labour and economic statistics do not capture the performance of the music business well because the classification of economic statistics dates to the 1960s. Two key elements of a musician’s work - live performances and sound recordings - are in different economic classes. Composer-performers, the typical musicians of popular music do not fit into these categorisations. Adding to this complexity, the frequent presence of other artistic, technical, managerial or educational functions makes a musician’s work hard to categorize.

The complexity of a musician’s work makes professional training very challenging, too. Popular music throughout the world is mainly learned in informal settings. However, this is not the ideal setting to learn the necessary managerial, economic, legal and other skills that are necessary to fulfil the freelance job of a professional musician.

4.2 How We Define the Music Industry?

The three income streams model is a value chain based model developed in the United States (Hull et al. 2011) and adopted by the European Commission’s Joint Research Center for European CCI policy purposes (Leurdijk and Ottilie 2012). We made minor adaptations in the three income model for applicability in less developed markets in Central and Eastern Europe.

While in the original American model sound recordings are the “main” income stream, currently, especially in Central Europe the live performance stream earns the most income for a typical musician. The author’s stream is the oldest, traditionally and analytically first part of the music industry that includes revenue streams based on musical works exploited by music publishers and via author’s CMO societies. In the US it is called the publishing stream, but in Central Europe it is dominated by authors’ societies, so we modified the label to ‘author’s stream’.

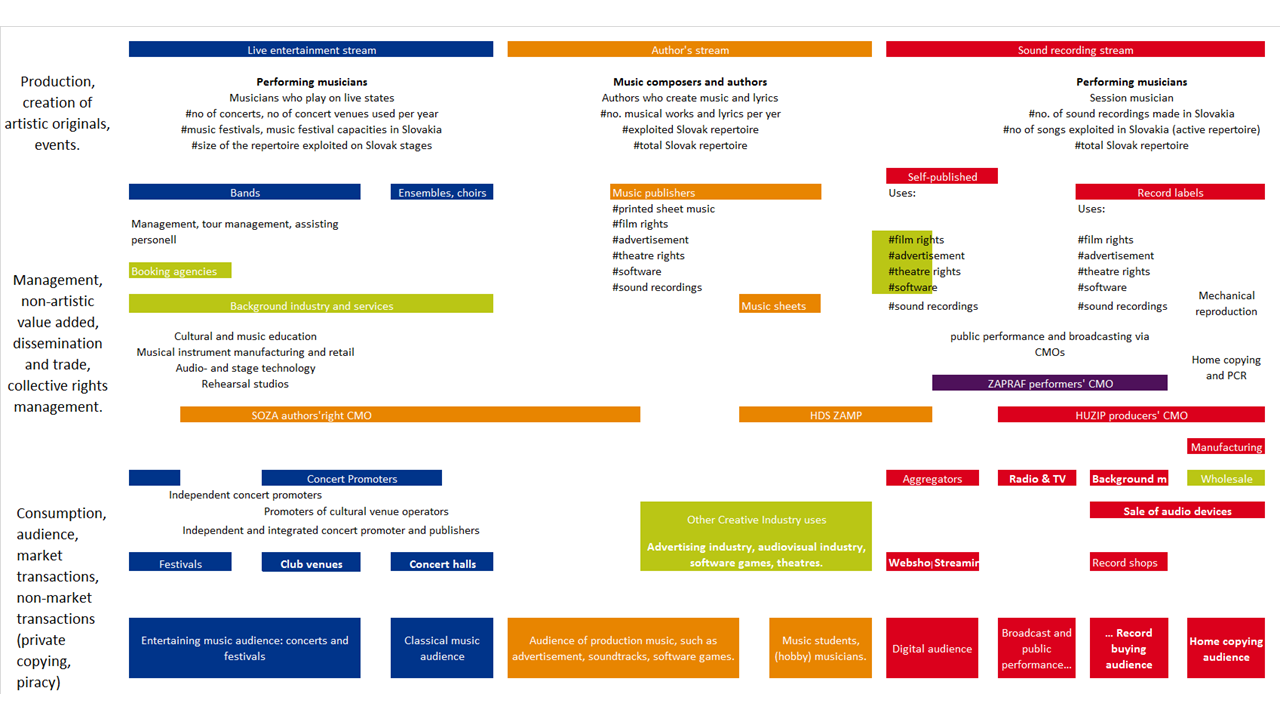

Figure 4.1: The Thee Income Streams

The music industry became divided in 1909 when the U.S. Supreme Court denied copyright protection for phonographic rolls. The phonographic industry which changed from rolls to record plates and later to CDs and digital albums sought intellectual property protection. The exploitation of these neighbouring rights created separate revenue streams for record producers and self-published musicians. From the 1930s the recording industry far surpassed the music publishing business worldwide and became the dominant revenue source for the whole industry until the 2000s.

Through the 2010s the live performance stream created the most revenues in many developed and emerging markets, and it is especially important in Central Europe. It has an exceptionally strong input to employment, given that live performances create jobs in transportation, in the venues and the connecting accommodation, food and beverages industries, where many enterprises cannot serve their clients without live or recorded music. Food and beverage services are the second largest European employer after construction and its tourism-related segment is also a large service exporter. Unlike the other two streams, live performances do not receive, but pay musical royalties to authors. Neighbouring rights are not involved unless the live performances are recorded and published in audio or audiovisual recordings.

4.3 What Is Unique in Our Survey? How Does it Relate to Other Industry Data Sources and Issues?

Our music professional surveys are designed to collect information that is not available in other music industry sources, targeting three groups: the artists, the technicians, and managers.

CEEMID uses Music Professional surveys to understand working conditions, skills, remunerations, concert economy, granting. Statistical data, such as unemployment, average wage or GDP data is mainly produced by statistical reporting, anonymized tax returns data and mandatory financial statement data by the national statistical authorities.

4.3.1 Other Industry Research

In live music, there are very few comprehensive data sources in Europe, and they are very hard to access and integrate. Live DMA collects data in order to analyze the situation of live music venues and clubs in Europe. Their survey program is excellent, but only covers some aspects of live music and only in a small number of countries, which had not overlapped so far much with CEEMID’s. The two surveys greatly complement each other, because we survey the individuals who use the venues for their projects, while they ask the venue managers. We ask about the costs and revenues of the projects that are hosted in venues, and they ask the venues themselves. For users of LIVE DMA survey, our data just fills out the a lot of gaps. In European countries where LIVE DMA has not yet set foot, our surveys may be the only data source on the live music economy — the part of the music business that created the most income in the 2010 and which was shut down by the pandemic.

Our survey also complements IFPI’s data resources on the recording industry. IFPI collects data via its national affiliates from labels. Our research shows that this usually omits a smaller, self-published segment, which is not significant in market value but significant in recording output. However, our survey also goes further ‘upstream’ in the value chain, for example, asking about recording costs.

We also complement CISAC’s data collection program. After the Commission v CISAC case (InfoCuria 2013) the authors’ societies international organization stopped collecting and disseminating any pricing related information. In our view, this was too cautious an overreaction, and put especially smaller member societies into a very difficult position. Our surveys (and other CEEMID data sources) aimed to help CISAC’s members in evidenced-based valuations, helping to resist downward pressure on prices.

Grant managers often have a duty to collect survey data for ex post grant evaluation. We give a general framework mainly for ex ante grant evaluation (i.e. making sure that a forthcoming grant call is suitable for the target audience) but we also collect high-level data that may be used as a starting point of ex post grant evaluation.

4.4 HR & Lifelong Training

In our view, the greatest challenge of the music industry is the lack of any strategic HR function in most of the industry. This means that music professionals hardly have access to life-long learning. Before the pandemic, the markets we analyzed were plagued by structural unemployment: many people were complaining that they do not get enough paid jobs, while employers were complaining that they do not find reliably skilled freelancers of employees. The music industry is a high-value added industry that mainly adds value to the economy via its labour force. We try to collect data that may help the industry to manage better the education and vocational training of the industry.

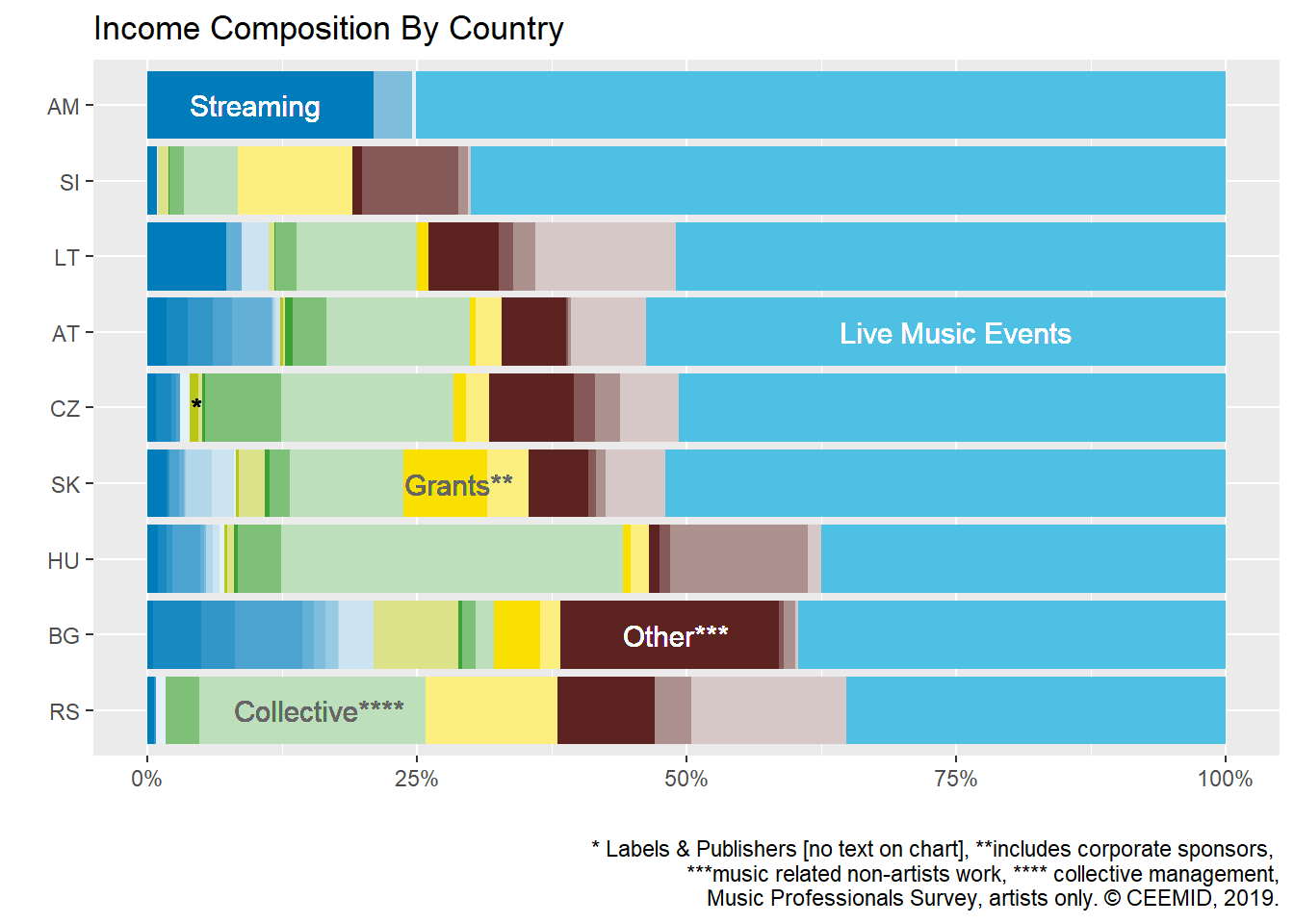

Figure 4.2: Taken from our Central European Music Industry Report 2020

And at last, but not least, our surveys target individuals which allows us to understand the structural changes in the industry. Before the COVID-19 pandemic we realized that in some markets, the publishing side became so much more valuable compared to the recording side that publishers started to invest into sound recordings. Obviously, these trends are not well captured by either the recording industry’s and the publishing side’s very different data sources. Our approach gives the live music, recording industry, publishing and grant managers a comprehensive view that also shows how their roles are defined in relation to each other. (See Chapter 3 The Creation of Music in our CI-CEEMID Central European Music Industry Report for an example.)

4.5 Relationship to Audience Surveys

Our surveys are collecting data from the supply of the industry, while audience surveys are collecting data from the demand side. When the concert or recording market is in balance, some information can be analyzed with only collecting data from the supply or demand side. For example, price should be the same, regardless of whether we ask those who pay or those who get paid.

Unfortunately, the music industry is not in a long-term balance. We used demand-side surveys to understand and get private copying compensated, for example. For the live music industry, we analyzed which demographic/geographical groups do not have access to live music, and currently, we should ideally know how fans keep in touch with their favourite bands and artists.

References

Hull, Geoffrey P., Thomas W. Hutchison, Richard Strasser, and Geoffrey P. Hull. 2011. The Music Business and Recording Industry Delivering Music in the 21st Century. New York: Routledge. http://search.ebscohost.com/login.aspx?direct=true&scope=site&db=nlebk&db=nlabk&AN=345262.

InfoCuria. 2013. “T-442/08 CISAC V Commission.” http://curia.europa.eu/juris/liste.jsf?num=T-442/08&language=EN.

Leurdijk, Adnra, and Nieuwenhuis Ottilie. 2012. “Statistical, Ecosystems and Competitiveness Analysis of the Media and Content Industries. The Music Industry.” 25277 EN. Edited by Jean Paul Simon. Luxembourg: Publications Office of the European Union, 2012: Joint Research Centre Institute for Prospective Technological Studies (IPTS). http://ftp.jrc.es/EURdoc/JRC69816.pdf.